VIETNAM CHAMBER OF COMMERCE AND INDUSTRY

Liên Đoàn Thương Mại Và Công Nghiệp Việt Nam

Sat, Aug 30, 2025, 15:51:00

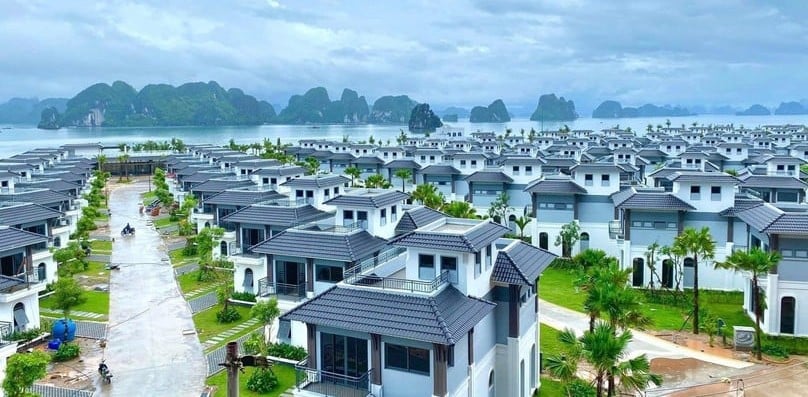

According to property consultancy firm DKRA Group’s July report, despite Vietnam's tourism rebound - welcoming over 1.5 million international arrivals in the first seven months, resort real estate continued to lag in its recovery trajectory. Demand and sales volume continued to underperform, hindered by high selling prices and unsold inventory.

Weak sales despite rising inventory

The report highlighted that only 45 units out of 2,268 vacation villas across 62 projects were sold during the seven-month period, equivalent to a modest 2% absorption rate.

Primary supply saw a slight year-on-year decrease of 1%, maintaining low levels. Although new supply increased 85% compared to the same period last year, the total volume remained far below pre-2022 figures.

Liquidity was low despite marginal improvement in buyer interest. Most transactions were concentrated in properties priced under VND10 billion ($379,506) per unit. The central and southern regions accounted for 74% of national supply, while the northern region led in absorption, making up 84% of successful transactions.

Primary market prices varied widely. In the North, listings ranged from VND4.9 billion to VND106 billion ($4.02 million) per unit; in the central region, from VND14.6 billion to VND134.4 billion; and in the South, from VND5.2 billion to VND155.7 billion per unit.

The resort shophouse segment was even weaker, with only six out of 3,448 units sold across 32 projects, representing a 0.2% absorption rate. Notably, 99% of available supply consisted of inventory from previous years. The central region led in supply with 67%, followed by the South (26%) and North (7%).

Prices for shophouses ranged from VND4.6 billion to VND34.2 billion ($1.3 million) in the North; VND6 billion to VND56.7 billion in the central region; and VND5.8 billion to VND70 billion in the South.

The condotel market fared similarly, with 29 units sold out of 4,464 available across 48 projects, a 1% absorption rate. The central region accounted for 64% of national supply, followed by the South (22%) and the North (14%).

Primary prices per square meter ranged from VND37.8 million to VND141.1 million ($5.35 million) in the North, from VND42.4 million to VND188.7 million in the central region, and from VND61.8 million to VND154.5 million in the South.

Incentives fall short, investor sentiment remains weak

Vo Hong Thang, chief investment officer at DKRA Group, noted that despite a strong rebound in tourism and aggressive promotional efforts from developers, market response has been underwhelming. Investor confidence remains low, and a near-term recovery in demand, liquidity, or price growth is unlikely, especially given unresolved legal uncertainties surrounding condotel ownership.

Similarly, Nguyen Hoang, deputy director of Eagle Academy, commented that a return to the “golden era” of 2016-2018 for resort real estate is highly unlikely. Many investors had expected tourism growth to directly translate into property gains but the current market paints a contrasting picture, marked by weak transaction activity.

Oversupply, haphazard development, high prices, and lack of regulatory clarity are among the key challenges. The resort property market may need a new catalyst - potentially the APEC 2027 Economic Leaders’ Meeting in Phu Quoc Island, the southern province of An Giang - to gain momentum.

On a more positive note, Nguyen Van Dinh, chairman of the Vietnam Association of Real Estate Brokers (VARS), pointed to expanded visa policies and ongoing infrastructure upgrades as potential drivers of recovery in key resort markets.

Tourism property values in the central city of Danang, Nha Trang town in the south-central province of Khanh Hoa, and Phu Quoc have gradually improved. While there have been no sharp price increases, the “cut-loss” trend has largely abated, with growing investor optimism. Some projects have even seen 5-10% gains in secondary market prices over the past year.

Simultaneously, a number of high-end resort developments have resumed construction or launched new sales phases, with several developers reporting positive early sales.

Dinh emphasized that visa waivers will encourage developers to release new inventory or revive stalled projects in tourism hotspots. Moreover, the growing influx of international visitors - characterized by longer stays and higher spending - will drive demand for premium products such as beachfront villas, international-standard resorts, and luxury condotels.

He also stressed the need for local governments to invest in critical infrastructure, including airports, seaports, and transportation links, to accommodate rising tourist numbers and unlock the full value potential of regional real estate markets.